About Insurer

The AutoAid and Autonational Membership Breakdown Plans are arranged and administered by Right Choice Insurance Brokers and underwritten by Right Cover Insurance Limited. Both companies are owned by Lucida Broking Holdings Limited.

Right Cover Insurance Limited is a Licenced Insurer registered with the Guernsey Financial Services Commission (GFSC) under the Insurance Business (Bailiwick of Guernsey) Law 2002. The Company is registered in Guernsey (Company Reg. No. 67921) and its registered office address is:

Second Floor, Block A, Lefebvre Court, Lefebvre Street, St Peter Port, Guernsey, GY1 2JP.

If you have a general enquiry, strictly in relation to your insurance policy only, please email:

rightcoverinsurance@strategicrisks.com

If you have a complaint regarding your AutoAid or Autonational Insurance Policy then you should contact us as described below. We aim to provide you with a high level of service at all times relating to the benefits provided by the AutoAid and Autonational Insurance Policies.

However, there may be a time when you feel that our service has fallen below the standard you would expect. If this is the case and you wish to complain, we will do our best to try and resolve the situation.

You can submit your complaint by writing to us:

If we are unable to resolve your complaint by close of business on the third working day after receipt, an acknowledgement will be sent confirming who is dealing with it and when you can expect to receive a response.

Within 8 weeks of the date the Insurer receives a complaint the Insurer will provide you with their final decision.

If you remain dissatisfied following the final response from the Insurer, you can refer your case to the Channel Island Financial Ombudsman (“CIFO”) within 6 months from the date of our final decision.

You can contact CIFO by the following methods:

At any time, you can request a copy of our complaints procedures.

This does not affect your right to take legal action. If you ask someone else to act on your behalf, we will require written authority to allow us to deal with them.

You are not eligible to claim under the UK Financial Services Compensation Scheme (‘FSCS’) which is available to UK registered insurers. Right Cover Insurance Limited is a Guernsey registered insurer and FSCS therefore does not apply.

The directors are responsible for the maintenance and integrity of the corporate and financial information on the Company website. Legislation in Guernsey governing the preparation and dissemination of Financial Statements may differ from legislation in other jurisdictions.

A copy of the latest (2025) Financial Statements for the Insurer can be found HERE. A copy of the 2024 Financial Statements for the Insurer can be found HERE.

Data Protection Notice

Please refer to your Autoaid or Autonational Insurance Policy which details how the Company will handle your data.

Public Disclosure

Profile of the Insurer

Right Cover Insurance Limited is a Guernsey-registered licensed insurer operating under the Insurance Business (Bailiwick of Guernsey) Law, 2002, and underwrites the AutoAid and Autonational breakdown insurance plans arranged and administered by Right Choice Insurance Brokers, forming the core nature of its business. Right Cover Insurance Limited maintains its registered office at Second Floor, Block A, Lefebvre Court, Lefebvre Street, St Peter Port, Guernsey, GY1 2JP. Both companies are owned by Lucida Broking Holdings Limited.

Right Cover Insurance Limited's activities are centred on underwriting motor-related breakdown insurance products, representing its primary business segment. The Insurer operates within the Guernsey regulatory environment under the supervision of the Guernsey Financial Services Commission (GFSC) and is not covered by the UK Financial Services Compensation Scheme (FSCS), reflecting the specific external environment in which it operates. The Company’s objectives include delivering high service standards, maintaining transparent communication, and ensuring full compliance with applicable legal and regulatory requirements, supported by robust complaints-handling processes designed to uphold regulatory expectations and maintain policyholder confidence.

Corporate Governance

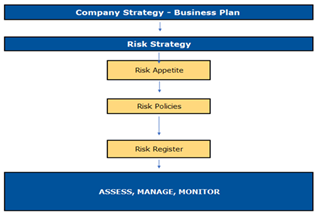

The Company adheres to Appendix 3 of the Finance Sector Code of Corporate Goverance which can be found HERE. A visual representation of the Company's Risk Management Framework is as follows:

Technical Reserves

Please refer to the "Critical Accounting Judgements and Key Sources of Estimation Uncertainty" note within the Company's financial statements for details of its approach to technical reserves.

Insurance Risk

Please refer to the "Insurance and Financial Risk Management" note within the Company's financial statements for details of its approach to technical reserves.

Financial Performance

The Company’s financial performance is driven by underwriting activity and investment returns. Earnings are influenced by premium volumes, claims experience, operating expenses, and the management of invested assets. Claims development is monitored to support the assessment of reserving adequacy, while pricing is reviewed to ensure premiums remain sufficient to cover expected claims, expenses, and risk margins. Investment performance reflects a prudent strategy focused on capital preservation and liquidity, consistent with the Company’s risk appetite and regulatory obligations.

Capital Adequacy

Solvency Requirements/Capital Adequacy

As part of its ongoing regulatory obligations, the Compay is required to meet certain solvency requirements as laid out in the Insurance Business (Bailiwick of Guernsey) Law, 2002 and underlying rules.

Minimum Capital Requirement

The Minimum Capital Requirement (“MCR”) set at 100% is intended to be the capital required to ensure that a licensed insurer should be able to meet its obligations over the next twelve months with an 85% probability. Further details in relation to the MCR achieved can be found in the notes within the financial statements.

Prescribed Capital Requirement

The Prescribed Capital Requirement (“PCR”) of a retail general insurer set at 135% is intended to be the capital required to ensure that the licensed insurer should be able to meet its obligations over the next twelve months with an 99.5% probability.

Further details in relation the PCR achieved can fe found within the financial statements.

Further information on the MCR and PCR can be found in The Insurance Business (Solvency) Rules and Guidance, 2021 on the Guernsey Financial Services Commission website HERE.

Financial Instruments

The Company holds a range of financial instruments that are used primarily to support its insurance operations, manage liquidity, and ensure the prudent investment of policyholder and shareholder funds. These instruments are managed in accordance with the Company’s investment policy, which sets out guidelines on credit quality, duration, diversification, and liquidity.

The Company’s investment objectives are to preserve capital, maintain adequate liquidity to meet policyholder obligations as they fall due, and generate stable risk‑adjusted returns. The investment policy is reviewed regularly by the Board to ensure that it remains appropriate to the Company’s risk profile, regulatory environment, and broader risk‑management framework.

Financial instruments are measured in accordance with applicable accounting standards, using valuation methodologies consistent with their classification. For assets measured at fair value, prices are obtained from independent pricing sources where available, with valuation techniques applied where observable market data is not present. The methods and assumptions used for measuring financial instruments for general‑purpose financial reporting are consistent with those used for solvency purposes unless otherwise disclosed.

Further information on the Company’s financial instruments, including a breakdown of investment categories, valuation methods, and associated risks, can be found within the relevant note to the financial statements.